Image generated in ChatGPT

WhatsApp UsIf you’re managing investments in Southeast Asia or Oceania, particularly through a private equity firm, investment fund, or family office in Singapore or Malaysia, you’ve likely noticed the growing emphasis on Scope 3 emissions.

You might see this as just another regulatory hurdle, but it offers one of the most significant opportunities to optimize portfolios in today’s market.

Let’s dive deep into what this means for your investments and how you can turn this challenge into a competitive advantage.

Understanding Scope 3 Emissions

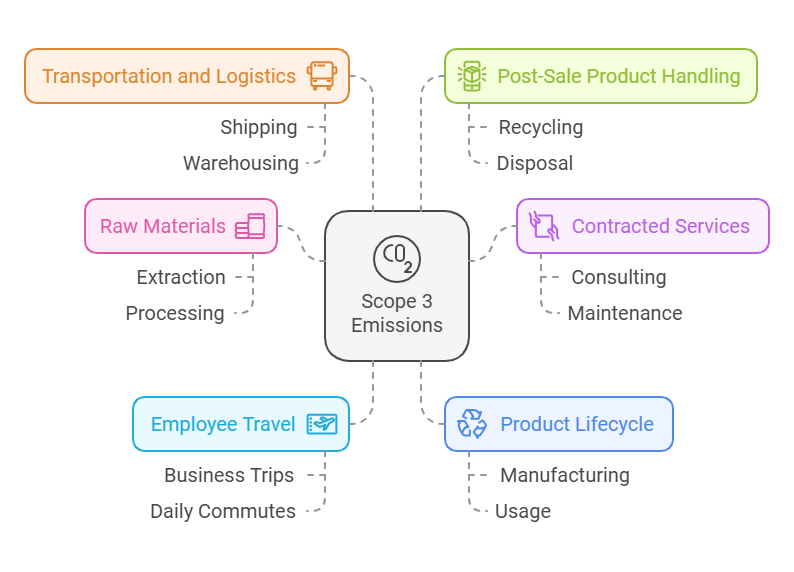

Scope 3 emissions might sound technical, but they’re essentially about understanding your complete carbon footprint story. While Scope 1 and 2 emissions cover direct operations, Scope 3 encompasses everything else in your value chain. Think of it as mapping out your entire business ecosystem’s carbon impact.

Let’s break down what we mean when we discuss Scope 3 emissions:

- Every raw material your portfolio companies purchase

- All the services they contract

- Employee business travel and daily commutes

- The entire lifecycle of products, from manufacturing to end-user impact

- The complex web of transportation and logistics across your supply chain

- What happens to products after they’re sold and used

Indirect emissions often make up over 70% of the total carbon footprint for most businesses in our region. Businesses must handle Scope 3 to go beyond compliance and focus on understanding and managing a major business risk.

McKinsey & Company states that these emissions can make up as much as 90% of a company’s total emissions, though the figure varies by industry. Additionally, the World Resources Institute notes that Scope 3 emissions typically account for about 75% of a company’s greenhouse gas emissions.

These insights show how significantly Scope 3 emissions affect a company’s overall carbon footprint.

Why Should You Care? (Hint: It’s Not Just About Being Green)

Why Should You Care? (Hint: It’s Not Just About Being Green)

Why Should You Care? (Hint: It’s Not Just About Being Green)

Why Should You Care? (Hint: It’s Not Just About Being Green)Regulatory Pressure

Regulators in Asia-Pacific are rapidly changing policies, and investors must stay ahead of these changes to succeed. Hong Kong’s HKEX and Australia’s ASX have mandated Scope 3 reporting starting in 2024, moving beyond mere suggestions. In our home turf:

- Singapore leads the way with its Carbon Pricing Act, implementing advanced carbon tax regulations and creating a robust carbon credits registration system

- Malaysia has launched its National Guidance on Voluntary Carbon Markets to help companies integrate emissions management into their strategies

- Regional stock exchanges increasingly demand climate-related disclosures

Investor Expectations

Businesses now recognize the Science-Based Targets initiative (SBTi) as the gold standard for credible net-zero commitments. Global investors now scrutinize companies’ comprehensive decarbonization plans, focusing on how they manage indirect emissions.

This isn’t just about checking boxes – it’s about demonstrating long-term viability to increasingly climate-conscious investors.

Risks of Greenwashing: The Carbon Credit Trap

Let’s talk about one of the biggest pitfalls in emissions management: overreliance on carbon credits. You can include carbon credits in a comprehensive strategy, but they shouldn’t serve as your primary solution. Here’s why:

The Right Way to Use Carbon Credits

- As a supplement to actual reduction efforts, not a replacement

- To offset hard-to-abate emissions while developing long-term reduction strategies

- Within a broader framework of science-based targets

Red Flags to Watch For

- Portfolio companies relying solely on credit purchases

- Lack of transparent reporting on actual emission reductions

- Absence of concrete plans for operational improvements

Renewable Diesel: A Pathway to Meaningful GHG Reductions

What Is Renewable Diesel?

Renewable diesel is a fuel that’s chemically identical to traditional diesel but produced from renewable resources such as agricultural waste, used cooking oil, and animal fats. Unlike biodiesel, it undergoes a hydrotreating process that ensures full compatibility with existing diesel engines, pipelines, and fueling infrastructure. This makes it a “drop-in” fuel that requires no additional modifications to vehicles or systems.

Environmental and Operational Benefits

Significant GHG Reductions

Renewable diesel can reduce lifecycle greenhouse gas emissions by up to 80% compared to traditional petroleum-based diesel. This reduction comes from both the renewable feedstocks and the cleaner burning properties of the fuel.

Improved Air Quality

It generates fewer particulate emissions and reduces harmful pollutants like sulfur oxides (SOx) and nitrogen oxides (NOx).

Operational Efficiency

Renewable diesel matches the energy density and performance of traditional diesel, ensuring no loss in vehicle efficiency or power.

Potential Impact on Scope 3 Emissions

Transportation—a significant component of Scope 3 emissions—is often difficult to decarbonize. Renewable diesel offers an effective pathway for companies aiming to reduce emissions in this category:

Logistics Operations

Switching fleet operations to renewable diesel can cut transportation-related emissions dramatically, with reductions of up to 80% in CO2 equivalents.

Supply Chain Decarbonization

By encouraging suppliers and logistics partners to adopt renewable diesel, companies can extend these benefits across their entire value chain. For example, freight and delivery services powered by renewable diesel contribute to lower upstream and downstream emissions.

Waste Utilization

Utilizing waste materials like used cooking oil as feedstocks for renewable diesel helps achieve circular economy goals while minimizing landfill emissions.

Case Study: Neste Corporation

Neste Corporation, a pioneer in renewable diesel production, exemplifies the fuel’s potential for decarbonization. Their “Neste MY Renewable Diesel” product has been adopted by various industries, including transportation and logistics, enabling companies to:

- Measure and Verify Reductions: Partners can track lifecycle emission reductions, aligning their actions with Science-Based Targets.

- Seamlessly Transition: By requiring no infrastructure changes, Neste’s clients can quickly adopt the fuel and immediately benefit from reduced emissions.

For instance, a global logistics company using Neste’s renewable diesel reported a 70% reduction in fleet emissions over a five-year period, showcasing the feasibility and impact of adopting this solution at scale.

Barriers to Adoption and Solutions

Cost Premiums

Renewable diesel typically costs more than conventional diesel. Governments can bridge this gap through subsidies, tax incentives, or carbon credit mechanisms.

Feedstock Availability

Limited availability of sustainable feedstocks can constrain production. Investments in feedstock innovation—like algae-based or synthetic options—can diversify supply.

Market Awareness

Companies may lack awareness of renewable diesel’s benefits. Outreach and education programs by industry leaders and policymakers can address this gap.

Making It Work: Your Action Plan

Investors play a critical role in reducing Scope 3 emissions by embedding sustainability within their investment strategies.

1. Due Diligence 2.0

During due diligence, they should evaluate portfolio companies’ Scope 3 emissions comprehensively, identifying key contributors and gaps in existing emission management practices.

Establishing ambitious yet achievable reduction targets aligned with frameworks such as the Science-Based Targets initiative (SBTi) provides a structured pathway for action.

2. Be an Active Owner

Active ownership and engagement are equally vital. Investors should encourage portfolio companies to adopt thorough Scope 3 accounting methods, ensuring that emissions data is accurate, comprehensive, and transparent.

Regular monitoring and reporting of progress allow for timely adjustments and maintain accountability, driving continuous improvement.

3. Build Your Network

Collaboration enhances the effectiveness of Scope 3 management. By fostering partnerships with industry groups, non-governmental organizations, and academic institutions, investors can facilitate knowledge sharing and the development of best practices.

Additionally, offering capacity-building initiatives, such as training programs, equips portfolio companies with the expertise to identify, measure, and mitigate Scope 3 emissions effectively.

4. Invest in Innovation

Innovation and technology investments are powerful levers for emissions reduction. Investors can prioritize funding for cutting-edge solutions, including renewable diesel production, carbon capture and storage technologies, and advanced supply chain analytics tools.

Supporting early-stage startups working on novel decarbonization solutions can also catalyze breakthrough developments, transforming industries over time.

5. Get Involved in Policy

Engagement with policymakers provides a broader avenue for impact. Advocating for supportive regulations and incentives, such as tax breaks for low-carbon technologies or subsidies for renewable energy, aligns market mechanisms with environmental goals.

Regional frameworks like the Singapore-Asia Taxonomy can serve as valuable tools for aligning investments with sustainability objectives, creating a robust foundation for sustainable finance.

By integrating these approaches into their strategies, investors can not only drive substantial Scope 3 emissions reductions but also enhance long-term portfolio resilience, deliver measurable environmental benefits, and contribute to global decarbonization efforts.

Success Stories to Learn From

Let’s look at some companies that are getting it right:

Comgest’s Smart Approach

Comgest, an asset management firm, has developed a robust strategy to incorporate climate considerations into its investment framework. They prioritize analyzing financed emissions, with a significant focus on Scope 3 metrics, to better understand the climate impact of their portfolios. By employing detailed carbon accounting tools, Comgest ensures that their investment decisions align with long-term sustainability goals.

In 2022, Comgest reported that over 65% of their actively managed funds were aligned with Paris Agreement trajectories, demonstrating their commitment to addressing climate risks.

Through targeted shareholder engagement, Comgest pushes portfolio companies to enhance their emissions reporting and adopt science-based targets, leading to measurable reductions in Scope 3 emissions.

Nippon Life’s Number Game

Nippon Life, one of Japan’s largest insurers, has embedded climate benchmarks into its investment strategies by systematically assessing companies’ GHG emission intensities, including Scope 3 metrics. Leveraging frameworks like the Paris Agreement, Nippon Life evaluates the alignment of corporate targets with net-zero pathways.

By 2023, Nippon Life had integrated climate risk analysis into over 75% of its investment portfolio. The company’s use of granular data allows it to guide investments toward organizations demonstrating credible decarbonization efforts, fostering accountability and resilience.

For example, in the automotive sector, Nippon Life’s investments have spurred automakers to disclose lifecycle emissions data and set ambitious electrification targets, directly addressing Scope 3 emissions.

Amazon’s Supplier Engagement Initiative

Amazon has taken a proactive approach to addressing Scope 3 emissions through its “Sustainability Exchange” program, launched in July. This innovative platform provides suppliers with essential resources to measure and reduce their emissions.

The program focuses on practical implementation, sharing detailed case studies and playbooks that help suppliers understand and act on decarbonization opportunities.

Walmart’s Financial Innovation

Walmart demonstrates how creative financing can drive supply chain decarbonization. Through its partnership with HSBC since 2021, Walmart offers suppliers favorable financing terms specifically for decarbonization initiatives.

Their Project Gigaton has achieved remarkable success, reaching its goal of helping suppliers avoid 1 gigaton of emissions six years ahead of schedule. This approach shows how large retailers can leverage their financial relationships to accelerate supply chain sustainability.

Schneider Electric’s Industry-Wide Impact

Schneider Electric has emerged as a pioneer in supply chain decarbonization, developing a comprehensive approach that extends beyond individual company relationships. Their sector-specific program, launched in 2021, initially targeted the pharmaceutical sector and has since expanded to include mining and semiconductors. The program combines educational programming with concrete decarbonization product offerings, actively working with more than 2,200 suppliers.

Schneider’s approach has yielded tangible results, particularly in renewable energy adoption. They’ve facilitated the formation of seven cohorts for joint renewable electricity purchases, demonstrating how collective action can make clean energy more accessible to smaller suppliers. This model shows how third-party expertise can catalyze industry-wide transformation in Scope 3 emissions reduction.

Unilever’s Supply Chain Revolution

Unilever, a global consumer goods leader, has implemented a transformative approach to supplier collaboration aimed at reducing Scope 3 emissions. The company’s “Climate & Nature Fund,” established in 2020 with an initial allocation of €1 billion, supports projects that drive decarbonization across its supply chain.

By incentivizing suppliers to adopt renewable energy and sustainable agricultural practices, Unilever has achieved significant progress. Between 2020 and 2023, Unilever reported a 23% reduction in Scope 3 emissions across its top 300 suppliers.

The company’s digital platform, which tracks supplier emissions data, ensures transparency and facilitates targeted interventions. By the end of 2024, they aim to have onboarded around 300 suppliers, accounting for approximately 44% of their Scope 3 GHG emissions related to raw materials, ingredients, and packaging.

Unilever’s efforts exemplify how collaboration and innovation can drive meaningful climate action within complex global supply chains.

The Local Regulatory Landscape

Investors operating in Southeast Asia and Oceania should stay informed about evolving carbon market regulations:

Singapore

Investors operating in Southeast Asia and Oceania must navigate a dynamic regulatory environment as governments intensify their climate commitments. Singapore has established itself as a regional leader by positioning itself as a carbon services hub.

With initiatives such as the implementation of standardized spot contracts for carbon credits and plans to develop carbon futures markets, Singapore is creating a robust framework to support market-based emissions reductions.

The city-state’s progressive Carbon Pricing Act enforces a carbon tax of SGD 25 per tonne, which is set to rise to SGD 45 per tonne by 2026. This structured pricing mechanism incentivizes businesses to adopt low-carbon technologies and aligns with Singapore’s broader Green Plan 2030.

Malaysia

In Malaysia, the government is committed to reducing its economy-wide carbon intensity by 45% by 2030, relative to 2005 levels, as part of its Nationally Determined Contributions (NDCs) under the Paris Agreement.

The launch of Malaysia’s Voluntary Carbon Market (VCM) Exchange in 2022 underscores the nation’s focus on fostering transparent and credible carbon offset mechanisms. By integrating emissions trading into its sustainability framework, Malaysia provides investors with clear avenues for engaging in decarbonization initiatives while ensuring alignment with international standards.

Indonesia

Indonesia has also made significant strides by introducing comprehensive guidelines for voluntary carbon markets. These guidelines emphasize transparency, integrity, and robust monitoring, reporting, and verification (MRV) processes.

Indonesia’s approach aims to leverage its vast natural resources, including forestry and mangroves, to generate high-quality carbon credits. These credits not only contribute to global emissions reduction but also provide economic opportunities for local communities.

As Indonesia positions itself as a major player in the global carbon market, it offers investors substantial opportunities to align with sustainable development goals.

The Bottom Line

Reducing Scope 3 emissions is an essential component of sustainable investment strategies. By integrating renewable diesel, mitigating greenwashing risks, and leveraging updated regulatory frameworks, investors can drive meaningful change.

Proactive engagement, innovation, and collaboration are key to achieving emission reduction targets and fostering a more sustainable future. Ready to take the first step toward comprehensive emissions management? Evaluate your portfolio’s Scope 3 emissions today!

Glossary

- Scope 3 Emissions: Indirect greenhouse gas emissions from a company’s value chain, including both upstream and downstream activities.

- SBTi (Science Based Targets initiative): An organization helping businesses set emissions reduction targets based on the latest climate science to align with the Paris Agreement.

- Greenhouse Gas (GHG) Emissions: Gases that trap heat in the atmosphere, contributing to global warming, such as CO2, methane, and nitrous oxide.

- Renewable Diesel: A sustainable fuel made from renewable sources like vegetable oils and animal fats, offering cleaner combustion than traditional diesel.

- Particulate Matter: Tiny particles or droplets in the air that can harm human health and the environment, often produced by combustion processes.

- SOx (Sulfur Oxides): Air pollutants formed when sulfur-containing fuels are burned, contributing to acid rain and respiratory issues.

- NOx (Nitrogen Oxides): Pollutants produced from vehicle and industrial emissions that contribute to smog and acid rain.

- Lifecycle Carbon Emissions: Total greenhouse gas emissions produced across the entire lifecycle of a product, from raw material extraction to disposal.

- Carbon Intensity: The amount of carbon dioxide emissions produced per unit of energy or economic activity.

- Supply Chain Emissions: Emissions generated through the production and transportation of goods and services within a company’s supply chain.

- Carbon Reduction: Efforts or measures aimed at decreasing the amount of carbon dioxide and other greenhouse gases released into the atmosphere.

- Transportation-related Carbon Emissions: Emissions from vehicles and transportation systems used to move goods or people.

- Environmental Footprint: The total environmental impact of an individual, organization, or product, including carbon emissions, water use, and waste.

- GHG Protocol: A widely used international standard for measuring and reporting greenhouse gas emissions across an organization.

- Paris Agreement: An international treaty aiming to limit global warming to below 2°C above pre-industrial levels, with efforts to limit it to 1.5°C.

References:

- https://assets.kpmg.com/content/dam/kpmg/my/pdf/uncovering-the-scope-3-opportunity-in-asia-pacific.pdf

- https://assets.bbhub.io/company/sites/63/2024/09/Case-Studies-on-Transition-Finance-and-Decarbonization-Contribution-Methodologies-Sep-2024.pdf

- https://assets.kpmg.com/content/dam/kpmg/sg/pdf/2024/11/unravelling-the-voluntary-carbon-market-in-sea.pdf

- https://www.mas.gov.sg/-/media/mas-media-library/development/sustainable-finance/singaporeasia-taxonomy-updated.pdf

- https://www.csis.org/analysis/clean-energy-and-decarbonization-southeast-asia-overview-obstacles-and-opportunities

- https://www.goldstandard.org/carbon-market-regulations-tracker

- https://www.tnb.com.my/assets/newsclip/18112024e.pdf

- https://www.pwc.com/sg/en/publications/assets/page/enabling-a-net-zero-world.pdf

- https://en.wikipedia.org/wiki/Carbon_offsets_and_credits

- https://www.reuters.com/sustainability/sustainable-finance-reporting/esg-watch-transition-credits-set-help-asia-shift-coal-2024-10-01/

- https://www.theverge.com/2024/8/1/24210744/climate-goals-corporate-watchdog-carbon-credit-offset

- https://www.reuters.com/sustainability/can-cop29-deal-clean-up-scandal-ridden-carbon-offsets-2024-11-18/

- https://unfccc.int/sites/default/files/NDC/2022-06/Malaysia%20NDC%20Updated%20Submission%20to%20UNFCCC%20July%202021%20final.pdf

- https://www.mse.gov.sg/faq

- https://www.unilever.com/files/8b5df5f6-cb90-40fd-9691-38d06905d81d/unilever-climate-transition-action-plan-updated-2024.pdf

- https://www.nissay.co.jp/global/report/pdf/tcfdtnfdreport_2024.pdf

- https://www.comgest.com/-/media/comgest/esg-library/esg-en/comgest-annual-sustainability-report.pdf

- https://www.neste.com/en-us/products-and-innovation/neste-my-renewable-diesel

- https://www.mckinsey.com/featured-insights/mckinsey-explainers/what-are-scope-1-2-and-3-emissions

- https://www.wri.org/update/trends-show-companies-are-ready-scope-3-reporting-us-climate-disclosure-rule

- https://time.com/7086071/supply-chain-decarbonization/

Need a reliable fuel or lubricant supplier in Singapore?

Interion supplies certified diesel, HVO renewable diesel, AdBlue and lubricants island-wide. Fast delivery, competitive pricing, technical support.

WhatsApp Us Now Enquire